SMM November 28: China's primary lead production saw a slight increase in November 2025, up 0.49 percentage points MoM but down 1.61 percentage points YoY. Cumulative primary lead production from January to November 2025 rose 7.06 percentage points YoY.

It is understood that as maintenance ended at several primary lead smelters, November production increased as expected, including in regions such as Inner Mongolia, Yunnan, and Hunan. However, during this period, lead smelters in Jiangxi and Anhui entered maintenance, unexpected maintenance led to production cuts at lead smelters in Yunnan in mid-to-late November, and smelters in regions like Hunan and Guangdong reduced output due to undersupply of raw materials, resulting in the final production increase falling short of expectations.

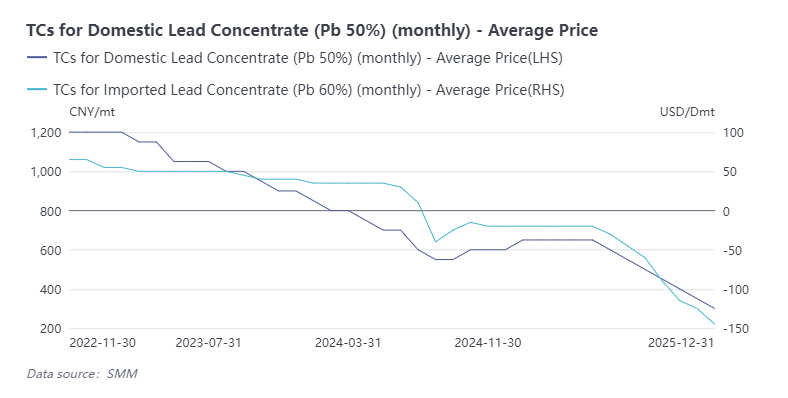

Entering December, maintenance at primary lead smelters increased MoM, primarily involving delivery brand enterprises, with output reductions distributed in Jiangxi, Yunnan, Hunan, and other regions. Meanwhile, smelters in Henan, Jiangxi, and other regions that underwent maintenance in November resumed production as planned, offsetting part of the production decline. Overall, SMM expects primary lead production in December to decrease by 1 percentage point MoM. Additionally, it is important to note that lead concentrate TCs fell further in December, with import ore offers as low as -$200/dmt, and the price trends of gold and silver were weaker than in October. Smelters' expectations for the value-added of lead concentrate by-products have decreased, and negotiations over lead concentrate TCs have reached a stalemate between mines and smelters. Subsequently, there is a possibility that smelters may further reduce output or fail to meet production increase expectations due to ore undersupply, potentially amplifying the production decline in December.

Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM's internal database model, and are for reference only, not constituting decision-making advice.

![[Analysis: With the End of Chinese New Year, How Will Primary Lead Enterprises' Production Fare in March?]](https://imgqn.smm.cn/usercenter/hrxHx20251217171721.jpeg)

![Geopolitical Boost to Nonferrous Metals SHFE Lead Rises on Fluctuations [Brief Review of Lead Futures]](https://imgqn.smm.cn/usercenter/mfCMp20251217171721.jpeg)